The Quiet Power of the Dollar

Financial Literacy, Community Wealth, and the Discipline of the Boycott

Wealth is not only what we earn.

It is how we decide.

Every dollar we spend is a choice about where power flows. It is a signal of what we tolerate, what we reward, and which systems we quietly sustain. In periods of political, cultural, or economic tension, people often ask what meaningful action looks like. Voting is periodic. Public protest is episodic. But spending is constant.

This essay explores how financial literacy, financial wellness, and the modern boycott intersect, not as ideology, but as an economic behavior. When understood clearly, boycotts are not about outrage. They are about capital allocation. And when practiced with discipline, they can strengthen individual financial health while reshaping community-level outcomes.

Financial Literacy Is Not Neutral

Traditional financial literacy education focuses on mechanics: budgeting, saving, investing, credit management. These are essential, but incomplete.

True financial literacy also requires understanding where money goes after it leaves our hands.

According to the U.S. Bureau of Economic Analysis (BEA), consumer spending account for roughly two-thirds of U.S. GDP. This means household spending decisions materially shape the broader economy.

From a wealth-building perspective, three truths matter:

Spending is economic participation, not neutrality

Collective spending patterns influence corporate incentives

Capital that leaves a community rarely returns on its own

Ignoring these realities does not make spending apolitical. It only makes it unexamined.

What a Boycott Really Is (and Is Not)

The word boycott often evokes emotion. Anger. Punishment. Protest.

Economically, a boycott is something more precise:

A coordinated reallocation of capital away from one actor and toward alternatives.

This distinction matters. A boycott that simply halts spending without redirection weakens the consumer. A boycott that moves spending creates competitive pressure and rewards alignment.

Economic historians studying the Montgomery Bus Boycott have long noted that its effectiveness came not from abstention alone, but from parallel systems that allowed people to keep moving, working, and spending elsewhere.

Historically, boycotts that succeed do so because they alter revenue trajectories, not because they dominate headlines.

Contemporary Capital Reallocation in Practice

In modern markets, many spending categories offer choice even when consumption itself is non-optional.

Telecommunications contracts, streaming subscriptions, and retail memberships are recurring revenue models. Small changes in customer behavior compound over time.

Research on subscription markets shows that customer churn, even at low percentages, has outsized financial impact because future revenue is lost alongside present revenue.

This is why values-based consumer decisions often focus on recurring expenses rather than one-time purchases. The leverage is structural, not symbolic.

The year 2025 alone offer multiple examples of values-based spending reshaping outcomes, without requiring ideological unanimity.

AT&T has faced consumer scrutiny tied to political donations and lobbying activity. In response, some customers chose to transfer monthly telecom spending to competitors. The impact here is not symbolic. Telecommunications contracts are recurring revenue streams, and churn directly affects valuation and investor confidence.

Disney operates within a subscription economy where consumer cancellations compound quickly. During periods of public controversy, even modest increases in churn have translated into material revenue pressure, reinforcing how sensitive subscription models are to consumer alignment.

Costco benefited from that redirection. Consumers did not stop spending. They relocated their spending to a company perceived as more aligned. Membership-based models amplify this effect, because each new member represents both immediate revenue and long-term retention.

Financial Wellness Comes First

The Wealth Salons holds a clear line:

You do not sacrifice personal financial stability for collective ideals. You integrate them.

Values-based spending fails when it:

Increases debt

Reduces access to essential services

Relies on impulse rather than comparison

It succeeds when it operates like any other financially literate decision.

The Federal Trade Commission (FTC) consistently emphasizes comparison shopping and informed switching as core consumer protections. The same skills apply here.

A disciplined approach looks like this:

Audit recurring expenses

Identify comparable alternatives

Compare total cost, not just price

Make one declared decision

This is not moral performance. It is financial agency to have economic dignity.

How to communicate it

Share information, not shame

Normalize intention over perfection

What decision can be declared now

“My spending will align with my values and my financial health.”

This is not moral purity. It is economic agency.

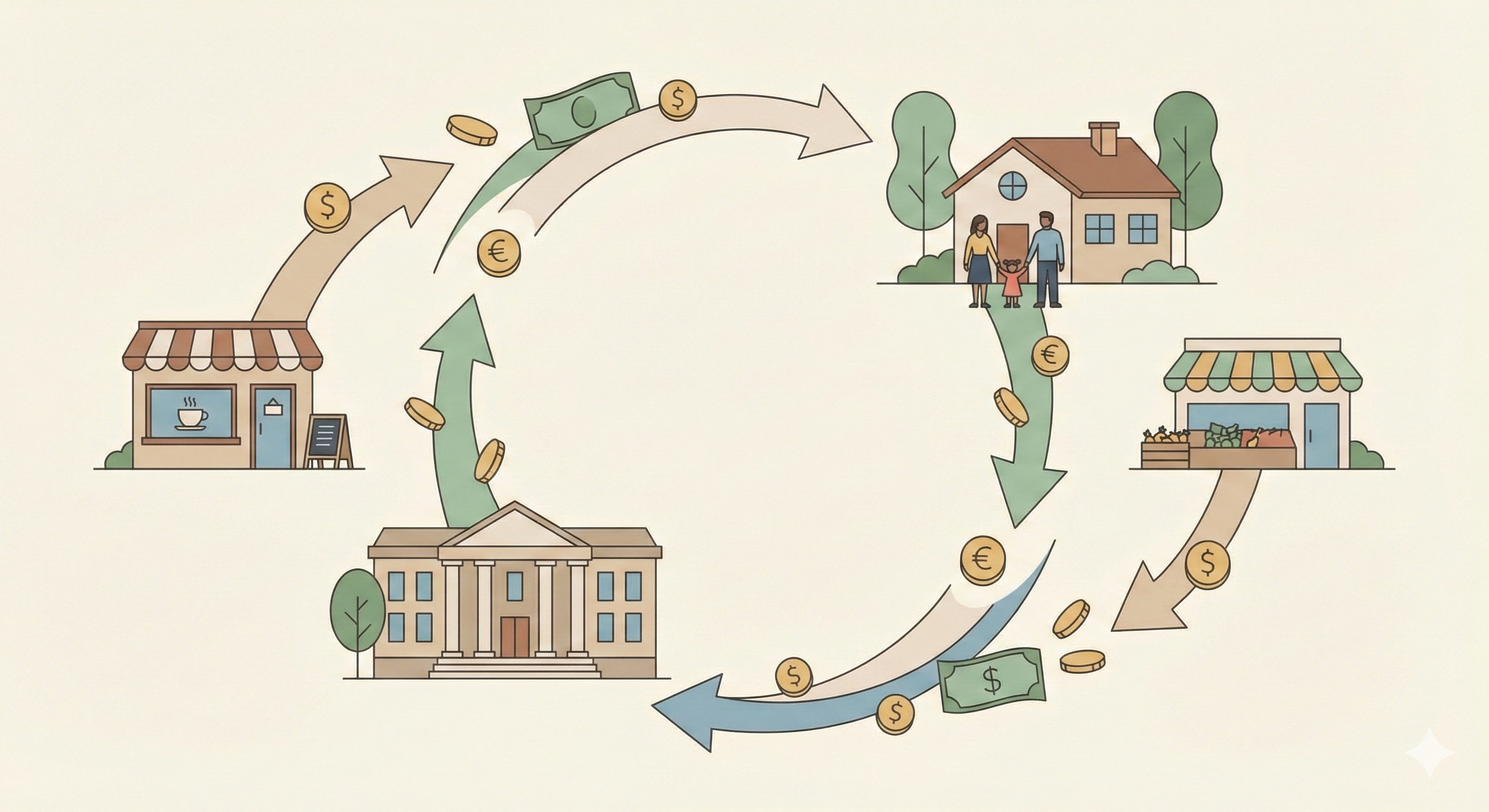

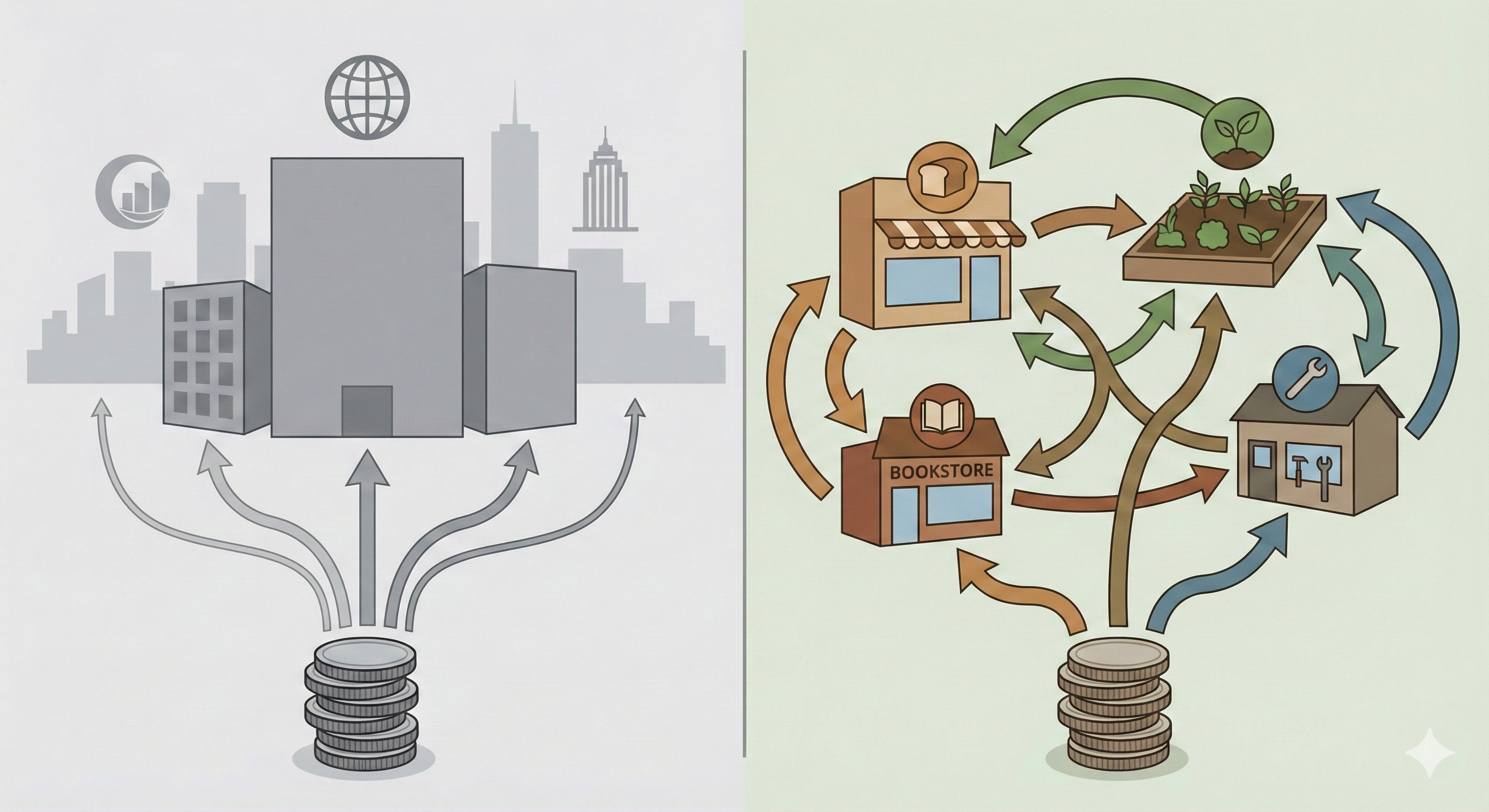

Community Wealth Is Built Through Retention, Not Abstinence

One of the most overlooked insights behind effective boycotts is this:

Wealth grows where money stays.

Economic development research shows that money spent locally circulates more times within a community than money spent with distant firms, increasing local income and employment effects.

When communities redirect spending toward aligned businesses, cooperatives, or institutions that reinvest locally, they shorten the distance between earning and compounding. This principle underlies everything from local procurement strategies to cooperative economics.

A widely cited meta-analysis from the Institute for Local Self-Reliance (ILSR) shows that local businesses return a significantly higher share of revenue to the local economy through wages, sourcing, and services.

Boycotts that simply reduce spending shrink economic activity. Boycotts that redirect spending can strengthen parallel economic systems.

This is why historically marginalized communities have emphasized cooperative economics, mutual aid, and shared purchasing norms. Not as protest theater, but as wealth retention strategies.

Make Informed Decisions

For readers who want to understand where consumer-led financial actions are emerging across industries, there are independent, community-maintained resources that track boycotts and spending redirections without requiring participation or agreement.

One such example is Cut Off the Spigot, which catalogs ongoing consumer actions and the stated rationales behind them. Resources like this are best used as information infrastructure, supporting individual evaluation rather than prescribing behavior.

Financial literacy includes knowing what exists, even when you choose differently.

The Quiet Audit

This month, identify one recurring expense.

Ask yourself:

Does this spending align with my values?

Does it strengthen or extract from my community?

Is there a comparable alternative that preserves my financial health?

Then make one declared decision.

Quietly. Intentionally. Without spectacle.